Days Sales Outstanding [DSO] is a measure of the average length of time your company takes to convert credit sales to cash. There is no magic number separating good DSO from bad DSO. To gauge the general health of your receivables, start by comparing your companies DSO with established industry benchmarks, but don't stop there. DSO is much more than simply a cash flow measure. Scrutinizing this ratio reveals much more than just how fast you're collecting. It also says a lot about the quality of your revenue and discipline of your business practices.

If you are struggling with a high DSO, you are struggling with a combination of one or more of the following: (1) Invoicing, (2) Collection efficiency, (3) Extended invoice terms, (4) Sales linearity.

Let's examine the ramifications of each.

Collection Efficiency - It is simply the ratio of cash collected divided by total cash collectible. It measures the effectiveness of your collectors and dunning process independently of other factors. Apart from negatively affecting working capital, continued slow collections ages your receivables, and requires you to book larger reserves that impact your bottom line. Not good. To increase collections efficiency, work on the following: (1) Strengthen relationships with your customers (2) Implement a pre-defined dunning timetable (3) Promptly escalate issues (4) Meticulously document all collection calls (5) Take appropriate legal measures early.

Collection Efficiency - It is simply the ratio of cash collected divided by total cash collectible. It measures the effectiveness of your collectors and dunning process independently of other factors. Apart from negatively affecting working capital, continued slow collections ages your receivables, and requires you to book larger reserves that impact your bottom line. Not good. To increase collections efficiency, work on the following: (1) Strengthen relationships with your customers (2) Implement a pre-defined dunning timetable (3) Promptly escalate issues (4) Meticulously document all collection calls (5) Take appropriate legal measures early. {kind=link}

Extended Terms - For sales people, granting extended terms is like throwing in the extra free knife to close the deal. However, this may really be indicating that extra incentives are needed to sell your products. The explicit cost of capital associated with extending terms is real and measurable; no biggie. Far more considerable, most analysts agree, is that increasing credit terms is a leading indicator of declining future sales revenue. Yikes! Remember also, average invoice terms are your DSO floor.

Extended Terms - For sales people, granting extended terms is like throwing in the extra free knife to close the deal. However, this may really be indicating that extra incentives are needed to sell your products. The explicit cost of capital associated with extending terms is real and measurable; no biggie. Far more considerable, most analysts agree, is that increasing credit terms is a leading indicator of declining future sales revenue. Yikes! Remember also, average invoice terms are your DSO floor. {kind=link}

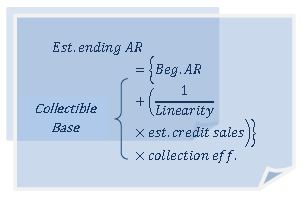

Sales Linearity - Having a disproportionate amount of sales occur near the end of the reporting period says your customers can wait to buy what you sell. For organizations using a sales channels model, this means you are likely 'stuffing' sales partners to satisfy top line revenue expectations. Consequently, margins (and sales people) get squeezed as customers and distributors wait for deals near quarter end. You have unwittingly lowered market expectations, and your high DSO is beginning to affect your stock price! In most companies struggling with DSO, linearity is often the biggest culprit.

Sales Linearity - Having a disproportionate amount of sales occur near the end of the reporting period says your customers can wait to buy what you sell. For organizations using a sales channels model, this means you are likely 'stuffing' sales partners to satisfy top line revenue expectations. Consequently, margins (and sales people) get squeezed as customers and distributors wait for deals near quarter end. You have unwittingly lowered market expectations, and your high DSO is beginning to affect your stock price! In most companies struggling with DSO, linearity is often the biggest culprit. {kind=link}

To effectively manage DSO, analyze each component to see which cog needs grease. All too often, people concentrate all their effort on dunning their customers, completely ignoring the other factors. Also, design effective hand-offs between processes. For example, how will collections document and report found invoice errors back to billing? Lowering your DSO requires a balanced and collaborative approach. Here's an example of what I mean.

I once worked for a company who had a terribly high DSO. As the comptroller, I was charged with the responsibility to drastically lower it. For the president of the company, hiring a collection manager was the simple and obvious solution. However, additional headcount simply did not address the root cause of our problem. His 'strategy' had a low probability of being effective because it only addressed 25% of the problem, at best. My pitch, which attempted to convince him of a four pronged approach, was agreed to reluctantly. Here‟s how it shook out.

{kind=link}

My first step was to understand our business processes, from sales to collection. I got involved with the invoicing process to get an idea of when and to whom our sales force was extending credit beyond normal terms. I wanted to understand our sales process to find out why 70% of our sales occurred in the last month of the quarter. Finally, I made myself a collector to understand why customers did not pay their invoices on time.

I decided to phone a list of customers that had invoices drastically overdue to see if I could strong arm the money out of them. To my amazement, I found that 8 out of the 10 customers I contacted had a total of 16 billing issues with the unpaid invoices. To make matters worse, they had already had the same conversations with our collections department. So, part of the problem was that our invoicing team produced erroneous invoices, and the only feedback mechanism to let them know this was through e-mails that were being largely ignored. A disciplined approach was needed. Creating a ticketing database that enabled our collectors to immediate communicate invoicing errors to billing was the solution. After agreeing upon SLA's, we saw a drastic reduction in invoicing errors. Collecting cash is much easier when you stop sending inaccurate invoices. We saw our DSO decreased considerably, but not to an acceptable point. We still needed to address the other factors.

{kind=link}

By in large, I found out our collectors were some of the best. Not since watching 'Bent Nose' Larry in action was I so impressed with cash collectors. As impressive as his methods were, my focus was much more on results. I used the 'collection efficiency ratio' to measure performance. Our collection efficiency was definitely not the issue. We were collecting over 95% of amounts due in the quarter. In one quarter, we were over 100%. That meant we collected amounts not yet due! Not bad. What also helped was goal setting. You can't really tell your collectors to ensure they hit the DSO target. Instead try calculating the desired collections needed to hit your DSO target. Remember to consider AR balances you brought in from the prior quarter, use current quarter expected credit sales, and back into the cash collections target.

Things seemed to be getting better, except our DSO. Our invoicing issues were solved, our collection efficiency was high, but our DSO was still too high? What was being neglected was our sales linearity. Our linearity came in consistently at around 33%. That is, we sold only 33% of our product in the first 2 months of the quarter. With standard 30 day terms, this meant that we had no chance to collect two-thirds of our credit sales before quarter end. Even at 100% collection efficiency, and no extended terms, the lowest we could get DSO down to was 60 days. It was obvious that sales linearity was the most disruptive element in our DSO reduction initiate. The most important thing now was to effectively communicate this to our sales organization. Many slide decks and meetings later, our sales organization was finally convinced they needed to address sales linearity, if not only to address DSO, but also to address margin gouging, and the strain put on operations to ship the majority of our product through a very tight window. We implemented a program of sticks and carrots for our channel partners to change their back-ended buying habits. It didn't happen overnight, but we eventually got traction.

Ah, a job well done… Not quite. I learned salesmen adapt very well to perceived obstacles. To combat this crazy notion of buying and paying for goods relatively evenly over time, they simply began extending terms. I imagine the pitch went something like this, "Just submit the order before the last month of the quarter and I'll extend the terms so payment isn't due until the next quarter anyway. Hey, you'll get your linearity rebate, and you keep your cash. Who loves you baby?" Bottom line, keep a constant eye on extended terms by developing a reporting mechanism to track them, and have them approved by someone outside the sales organization. Extended Invoice terms beyond 30 days all but disappeared once our CFO began signing off on all requests.

The old adage, 'Cash is King' still holds true. All too often companies get side tracked with a different objective than making money, giving way to top line revenue objectives that attempt to create shareholder value. Just remember, if you can't collect on those top line revenues, your share price will eventually suffer.

Apart from building solid DSO processes, here are some other recommendations.

- Use DSO as a Key Performance Indicator. Perhaps take it one step further and create a dashboard that displays the performance of each DSO factor separately.

- Know the factors negatively impacting your DSO and be prepared to discuss the factors with your analyst community.

- Set goals or SLAs and attach incentives and disincentives to each factor.

- Create cross functional teams. Managing DSO touches finance, sales, and operations.

- Remember, DSO is like steering a ship. Positive measures taken today take several quarters to see.

Visit www.cubexcel.com to see how your organization can take advatage of our software that enables users to populate dashboards like the 'DSO' in a matter of minutes.

Email sales@cubexcel.com or call 571.246.1560 to inquire about our products and services.